How to Create a Budget You Can Actually Stick With: 5 Simple Steps to Master Personal Budgeting

Do you feel like your finances are out of control? Struggling with credit card debt and wondering where you’ll find enough money to pay your bills? If this sounds familiar, creating a budget could be the key to getting your finances on track. In this article, we’ll guide you through five simple and effective steps for building a budget that you can actually stick to.

1. Track All Your Income and Expenses

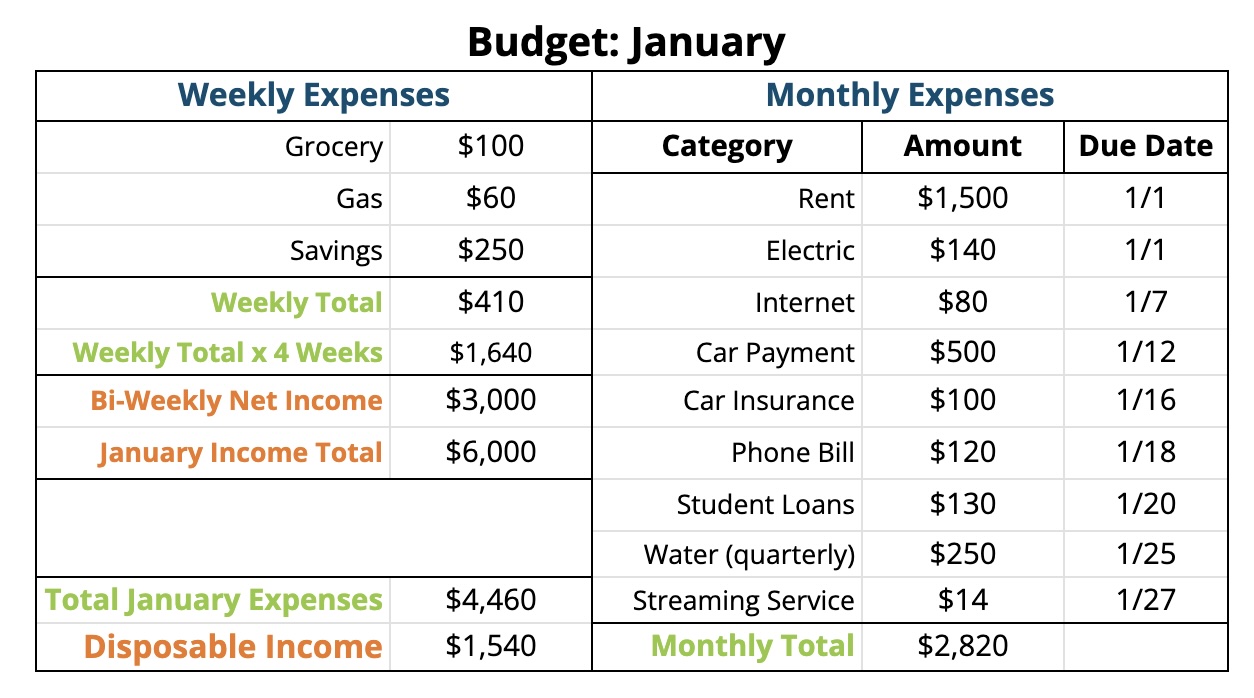

The first step to creating a budget that works is to understand where your money is currently going. Begin by tracking every cash and credit card expenditure for the next month on an expense tracker. You can use an Excel or Google spreadsheet, a budgeting app like Rocket Money, or the online tools available through your bank to help keep track. This process will give you an accurate picture of your financial situation and reveal areas where you can cut back.

Be sure to list all your monthly bills, including the names of each bill, the estimated amounts (e.g., $20 instead of $19.95), and due dates. Don’t forget to include quarterly or semi-annual expenses like real estate taxes, oil and water bills, or insurance premiums in your budget. Also, make sure to document your total monthly income and the sum of your bill expenses.

2. Calculate Your Disposable Income

Disposable income is the money left over after your monthly bills are paid. This amount can be spent on non-essential items, like dining out or entertainment. Your wants, not your needs. To find your disposable income, subtract your total monthly expenses from your total monthly income:

Total Monthly Income – Total Monthly Expenses = Disposable Income

If you find your discretionary spending too high, this is the first area to focus on when creating a budget. Look for opportunities to cut back on unnecessary purchases.

3. Reduce or Eliminate Unnecessary Expenses

Once you’ve assessed your disposable income, it’s time to look at ways to cut costs. Aside from reducing discretionary spending, consider canceling or lowering some of your recurring monthly bills. For example, you can cancel unused subscription services or look for cell phone and car insurance discounts. Log in to your account online or call your service providers to inquire about promotions or discounts that could help lower your monthly costs.

4. Prioritize Savings in Your Budget

When creating a budget, don’t forget to set aside money for savings. Allocate a specific amount to be saved from each paycheck, whether it’s $20 or $150 (or more). Make sure this savings amount is realistic and can be consistently put away. Savings should be considered a mandatory expense, just like your bills. Having existing savings can also help you cover planned or unexpected future expenses.

5. Make Sure Your Budget is Realistic and Sustainable

A good budget should be challenging, but not overly restrictive. While cutting back on unnecessary spending is important, don’t set yourself up for failure by eliminating all “fun” expenses. For example, cutting out dining out entirely may make you feel deprived, leading to impulsive spending. It then becomes easier to tell yourself that you already spent $20, so what’s $20 more?

Instead, budget for these “fun” expenses but at a reduced level. Can you save money on your daily coffee or reduce how often you eat out? By making small adjustments like these, you’ll stay within your budget while still enjoying some flexibility.

To help stay on track, continue using an online budgeting tool, which could link directly to your banking and bill payment accounts. Many apps and websites provide charts and visual breakdowns of your spending habits, giving you a clearer picture of your progress.

Bonus Tip: Stay Focused on Your Goals

A great way to stay motivated and committed to your savings goals is to visualize them. Hang up a picture or write down what you’re saving for—whether it’s an emergency fund, a vacation, or a new gadget. Keeping these goals in sight will help you stay focused and make it easier to stick to your budget.

Conclusion

Creating a budget is essential for taking control of your finances and achieving your long-term financial goals. You can build financial stability and reduce stress by tracking your spending, cutting unnecessary costs, prioritizing savings, and maintaining a realistic budget. Stick with these steps, and soon you’ll be on your way to mastering budgeting and improving your overall financial health.

Do you have a meaningful goal that feels out of reach, or aren’t sure where to begin? At Finivi Inc., our team provides comprehensive guidance to help you achieve your financial goals—whether it’s budgeting, saving, college planning, retirement, or any other financial or lifetime milestone.

Take a moment to complete this form or call us at (508)-870-0440, and we’ll help you find the best path to achieving your financial goals!

Disclaimer: The information provided is for informational purposes only and does not constitute financial or legal advice. Finivi Inc. makes no representations regarding the accuracy or completeness of linked third-party content and assumes no responsibility for any outcomes resulting from its use. External links do not imply endorsement. Please consult a professional before making financial decisions.

You must be logged in to post a comment.