By law, you’re entitled to three free credit reports each year. If you want more frequent access, Credit Karma offers free, regularly updated credit reports and credit scores from two major credit bureaus: Equifax and TransUnion.

You can view your credit information anytime with a free Credit Karma account. This allows you to monitor your credit, catch potential issues early, and make informed decisions to improve your financial health.

Here’s how to navigate and understand your credit report using Credit Karma.

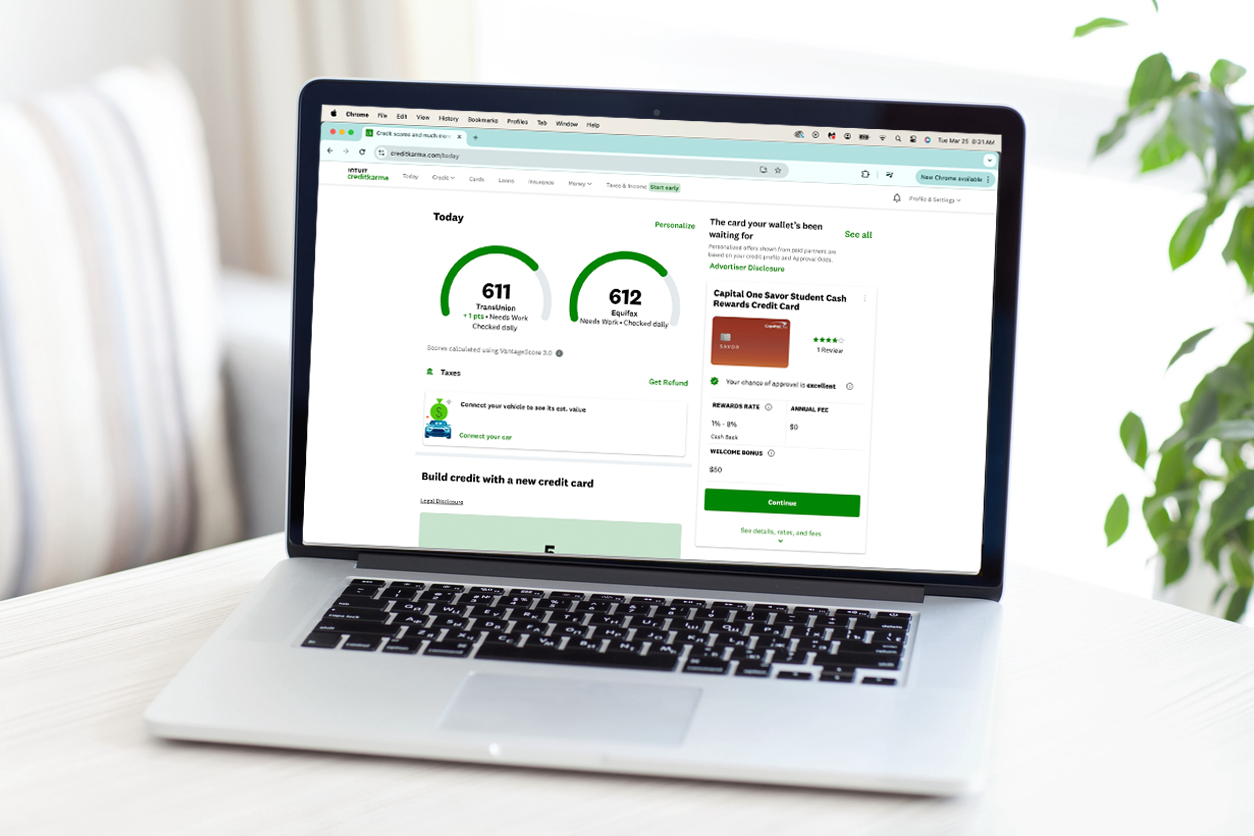

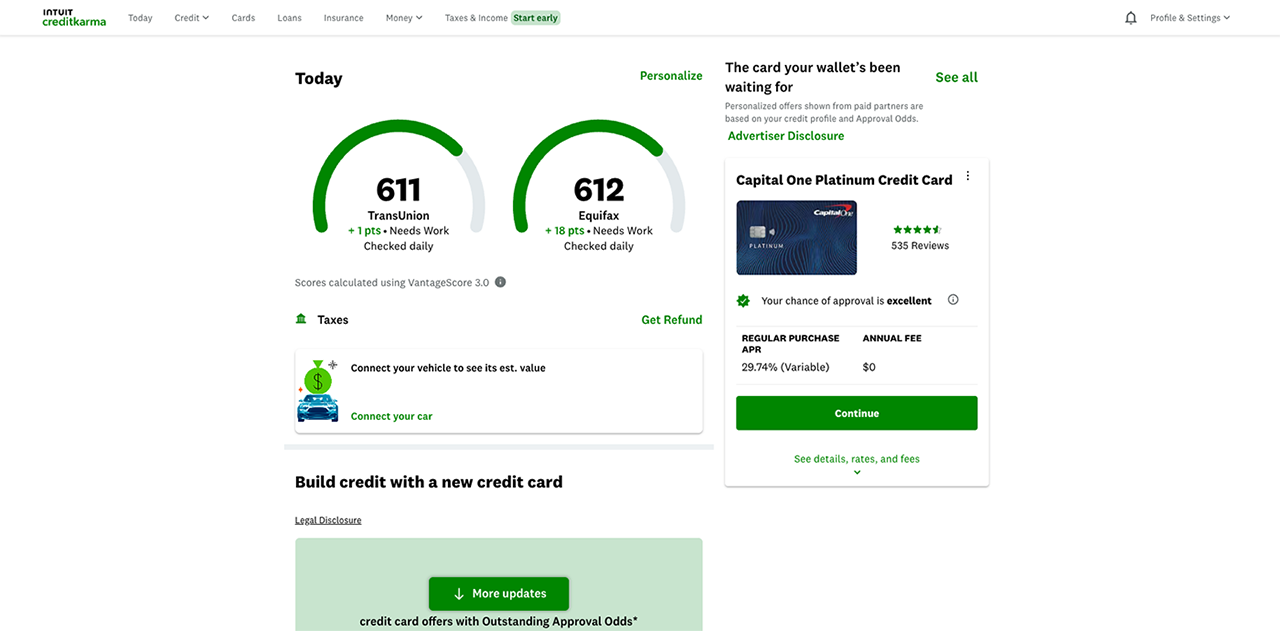

Navigating the Credit Karma Dashboard

You’ll land on your personalized financial dashboard once you log into your Credit Karma account. At the top, you’ll see your current VantageScore 3.0 credit scores from Equifax and TransUnion.

Clicking either score brings you to your Credit Health Report, where you can explore the factors influencing your credit score.

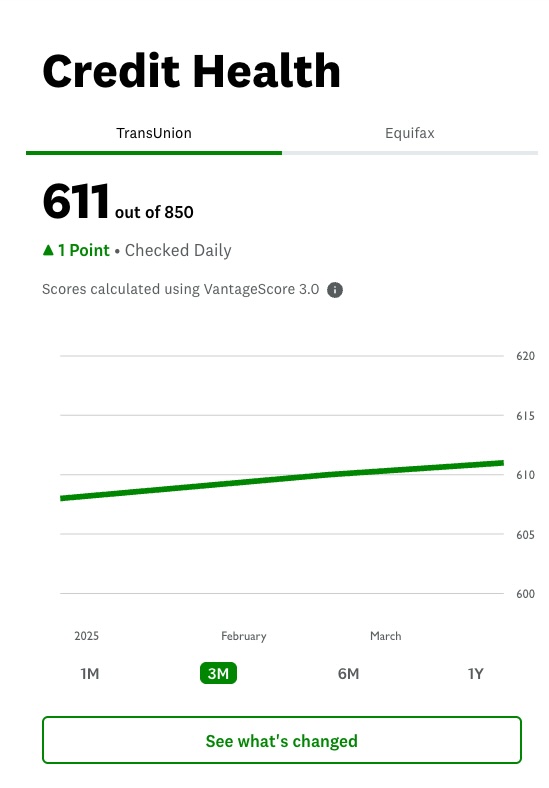

Understanding Your Credit Health Report

Your Credit Health Report includes a visual graph showing how your credit score has changed. At the top, you can toggle between your TransUnion and Equifax scores to compare them.

Clicking ‘See what’s changed’ opens a page that lists recent updates affecting your score, such as an increasing or decreasing student loan balance.

Below the graph is a breakdown of your Credit Factors, or the key components influencing your score. This list includes payment history, credit card use, derogatory marks, credit age, total accounts, and hard inquiries.

Scrolling down the Credit Health Report page will lead you to the button to view your full credit report in greater detail.

At the bottom of the Credit Health Report, Credit Karma provides helpful links that answer common questions about credit scores, scoring models, and the differences between credit bureaus. These resources are especially useful if you’re new to credit or looking to better understand how your score is calculated.

Key Credit Factors (What Affects Your Credit Score)

Credit Karma breaks down your credit score into six key factors that determine the quality of your credit score. Each factor is labeled with a level of impact ranging from high to low, with a color-coded rating system to help you quickly assess where each aspect of your credit report stands:

-

- Green: Excellent

- Yellow: Fair

- Red: Needs work

Click on each factor listed on your Credit Health Report page for more details behind the values displayed. Here’s a closer look at what each credit factor means and how it’s measured:

Shows the percentage of credit and loan payments you’ve made on time. This is one of the most important factors affecting your credit score, so even a single late payment can make a noticeable impact. On the Payment History page, you will see helpful facts on calculating this metric and which types of late payments can hurt your score the most.

Here is how your payment history is typically rated:

-

- Green: 99% or more

- Yellow: 98%

- Red: Below 98%

-

Credit Card Use (High Impact):

Reflects how much of your available credit you’re currently using, also known as your credit utilization ratio. On the Credit Card Use page, you will see helpful facts on calculating this metric and tips for lowering your credit utilization ratio. Scroll down to view a list of open credit card accounts with their respective balances, limits, and individual credit utilization ratios. Click each one to get detailed information on your history with that card.

Here is how your credit card use is typically rated:

- Green: Less than 30%

- Yellow: Between 30% and 49%

- Red: 50% or more

-

Derogatory Marks (High Impact):

Indicates the number of serious negative entries on your credit report, such as collections, bankruptcies, or foreclosures. On the Derogatory Marks page, you’ll also find helpful facts on how this metric is calculated and what steps you can take if you have a collection or a public record.

Here is how your derogatory marks are typically rated:

- Green: Value is 0

- Yellow: Value is 1

- Red: Value is more than 1

-

Credit Age (Medium Impact):

Displays the average age (in years and months) of all your open lines of credit and loans. On the Credit Age page, you’ll find helpful information on calculating this metric and tips for maximizing your credit age.

Scroll down to view a list of open loans, credit cards, and other lines of credit, each showing the age of the account. Click on any listing to see your detailed history with that account.

Here is how your Credit Age is typically rated:

- Green: Value is 7 years or more

- Yellow: Value is between 5 and 6 years

- Red: Value is less than 5 years

-

Total Accounts (Low Impact):

Shows the total number of both open and closed credit accounts. Your Total Accounts factor will be marked either green or red based on how many accounts are in your credit history.

On the Total Accounts page, you’ll find helpful information about calculating this metric and what lenders typically look for regarding account variety and volume.

Here is how your total number of accounts is typically rated:

- Green: 11 or more accounts

- Red: 10 or fewer accounts

-

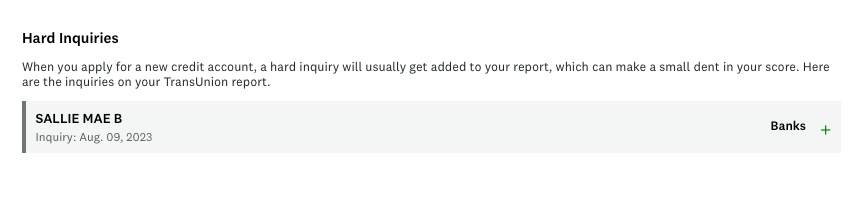

Hard Inquiries (Low Impact):

Reflects how many recent credit applications you’ve submitted, typically within the past two years. On the Hard Inquiries page, you’ll find helpful facts about how this metric is calculated and tips on how to keep your number of hard inquiries to a minimum.

Here is how your hard inquiries are typically rated:

- Green: Fewer than 3 hard inquiries

- Yellow: Between 3 and 4 hard inquiries

- Red: 5 or more hard inquiries

Your Credit Karma Credit Report

Under the Credit Report tab, you can view your full TransUnion or Equifax credit report. Here’s what you’ll find:

-

Personal Information:

Present and past names you’ve used, address history, and employment data reported to the credit bureau.

-

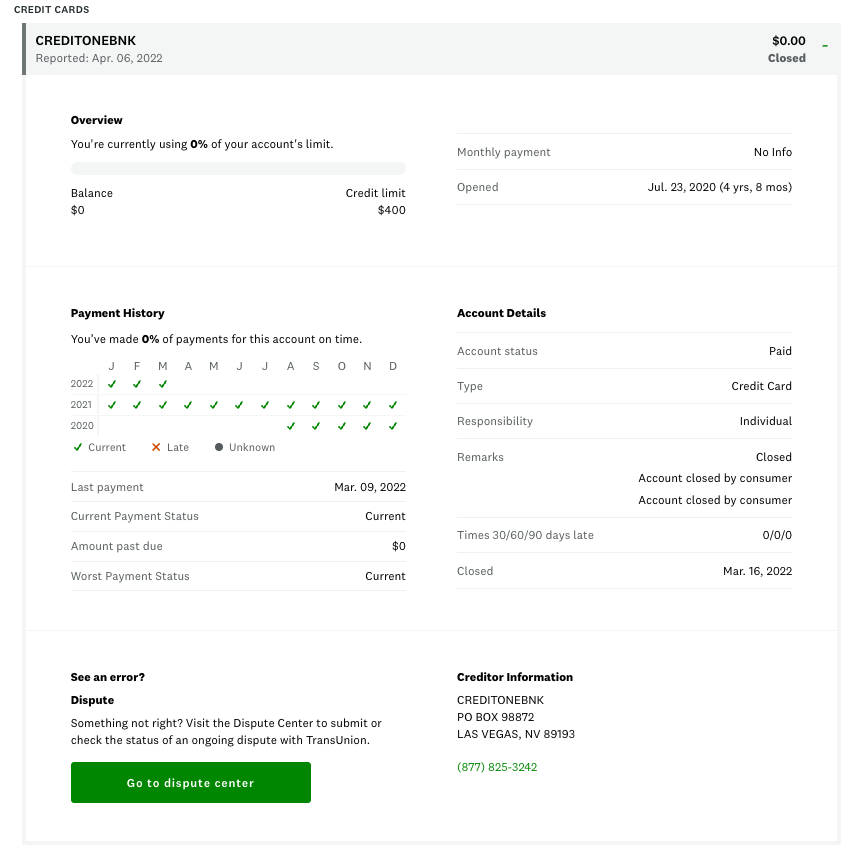

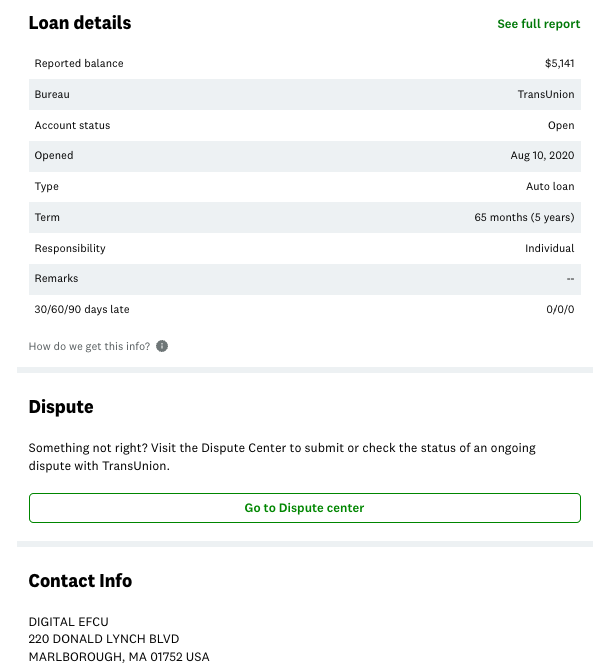

Accounts:

Includes loans, credit cards, and mortgages with status (open or closed), balances, whether the account is in good standing, the financial institution managing each account, and the date of the most recent account report.

Click on one of your accounts to expand and view additional information. Details may include your current balance, credit limit, date of last payment, date opened, loan term, whether the account is individually or jointly held, which payments were made on time (and which were late), the amount borrowed on a loan, the loan term, and more.

Found a problem with your data? Click the “Go to dispute center” button to report an issue to the credit bureau through Credit Karma.

-

Hard Inquiries:

Recent credit applications that can affect your score. An inquiry will only appear here if you’ve actively applied for a new loan or line of credit. Soft inquiries are not reported and do not impact your credit score.

-

Collections:

Debts sent to collections are shown here. Debt in collections stay on your report for up to 7 years.

-

Public Records:

This section shows a list of your bankruptcies, legal judgments, and matters of public record that can damage your credit score. Most records leave your report within seven years. Bankruptcies may stay listed on an individual’s report for ten years.

Chat With Penny

Use Credit Karma’s AI-powered assistant, Penny, to get instant answers about credit scores, reports, and common financial topics.

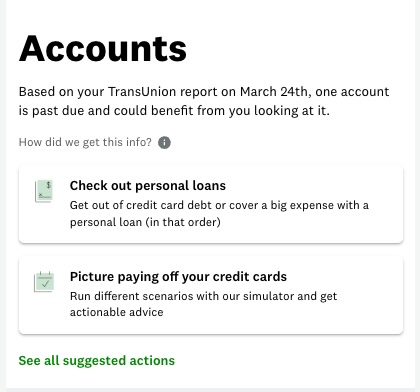

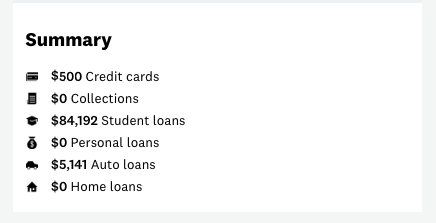

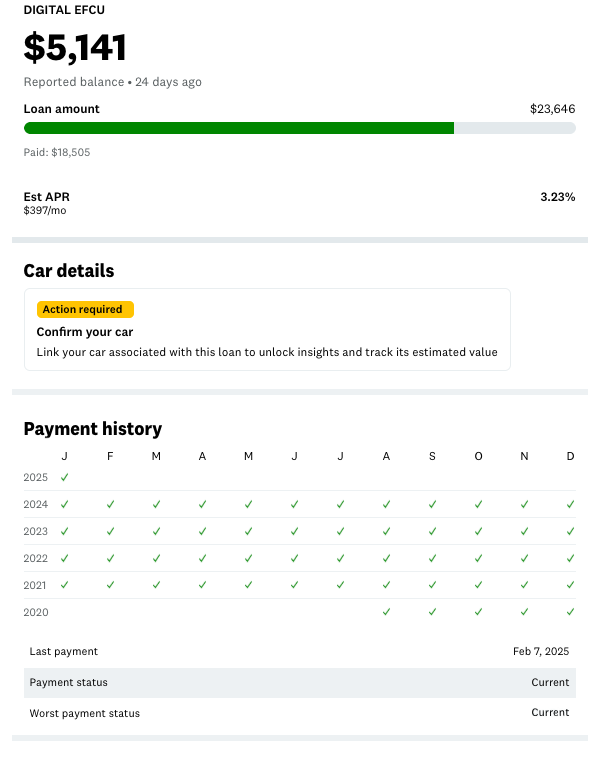

Using the “Accounts” Tab

A drop-down menu shows when you hover your cursor over “Credit” at the top of the screen. Select Accounts from that drop-down list to see a clear overview of the total amount you owe across each account (credit cards, student loans, home loans, auto loans, etc.). Alerts may appear at the top of the page to inform you that an account is past due or in collections with “suggested actions”:

On this page, you can see total reported balances, how much of each account balance you’ve paid off, and view a summary of your standing across all accounts.

Select an individual account to view more details on your credit or loan amount, estimated APR (Annual Percentage Rate), payment history, and additional loan details.

Other Credit Karma Tools

- Loan and credit card suggestions based on your data

- Tax filing services

- Auto marketplace hub (shop for car insurance, new and used vehicles, and view your motor vehicle records)

- Housing hub (explore mortgage tools and refinance options, find insurance, or a real estate agent)

Note: Credit Karma earns a commission when you use certain tools. That’s how they keep the core services free!

Final Thoughts: Why Reviewing Your Credit Report Matters

Accessing your credit report regularly through platforms like Credit Karma helps you:

- Build financial literacy

- Spot and dispute errors

- Improve your credit score

- Make better financial decisions

Understanding your credit is empowering; taking control of it is a smart step toward long-term financial wellness.

Disclaimer: This information is for educational purposes only and should not be considered legal or tax advice. Finivi Inc. makes no representations regarding the accuracy or completeness of linked third-party content and assumes no responsibility for any outcomes resulting from its use. External links do not imply endorsement.

Updated March 2025

You must be logged in to post a comment.