Secure Your Spouse’s Future: Understanding Survivor Benefits and Social Security Claiming Strategies

Coordinating Social Security benefits with your spouse is a key part of retirement planning. Many couples focus on maximizing their retirement benefits as soon as possible, but this approach often overlooks a critical factor: one spouse is likely to outlive the other. Making the right claiming decisions can ensure financial security for the surviving spouse.

Rethinking Social Security: The Safety Net vs. The Three-Legged Stool

Traditionally, retirement planning has been described as a “three-legged stool” supported by Social Security benefits, employer pensions, and personal savings. However, with fewer people relying on pensions, Social Security should be viewed as a financial safety net rather than a primary income source.

Recognizing this distinction can help couples make informed decisions, prioritizing long-term security over short-term gains.

How Social Security Survivor Benefits Work

Social Security survivor benefits provide the surviving spouse with their own primary or the deceased spouse’s benefit, whichever is greater. Unlike other Social Security benefits, survivor benefits are not subject to deeming rules, meaning a surviving spouse can claim them while allowing their own benefit to grow through delayed retirement credits.

However, the key factor is whether the deceased spouse had already claimed their benefits. The surviving spouse may have a reduced benefit if they claim early. This is why delaying benefits can be a crucial strategy for securing a higher survivor benefit.

The Impact of Delayed Retirement Benefits on Survivors

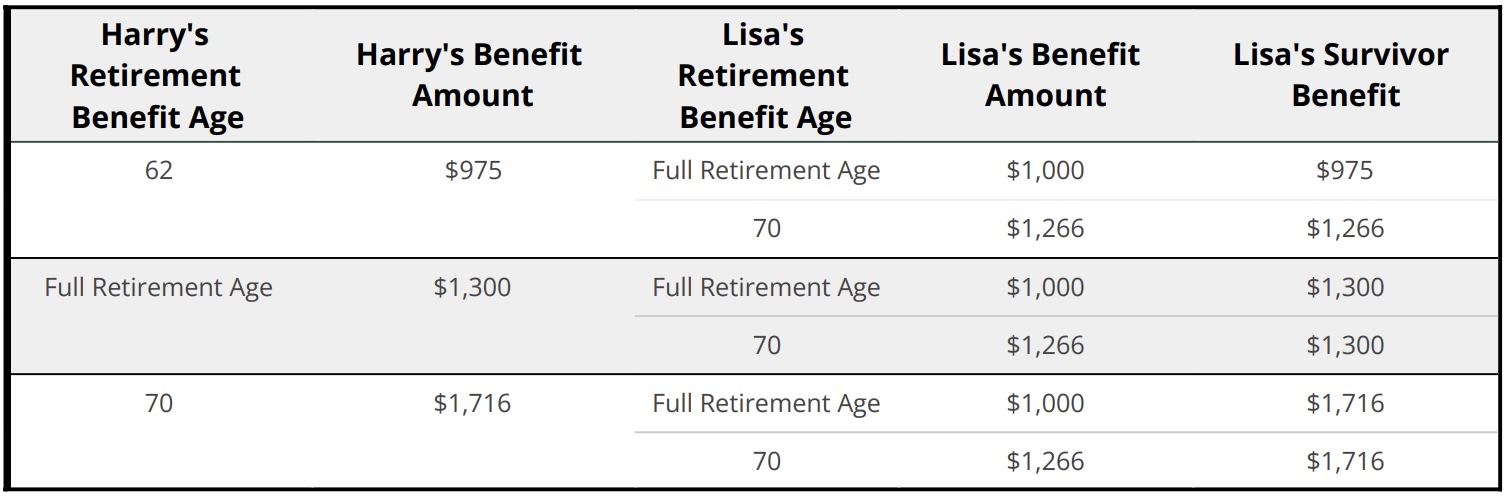

To illustrate, consider the case of Harry and Lisa:

- Harry (age 61) wants to take Social Security benefits at age 62. His full retirement benefit at his Full Retirement Age (FRA) would be $1,300, but at 62, it would be reduced to $975.

- If Harry delays his benefits until age 70, his monthly benefit grows to $1,716 with delayed retirement credits.

- Lisa (age 59) is eligible for $1,000 at her FRA. If she waits until age 70, her benefit would increase to $1,266.

- If Harry passes away, Lisa will receive the greater amount, her own benefit or Harry’s survivor benefit. The difference in amount depends on when each spouse takes his or her own retirement benefits.

The table below highlights how delaying Social Security benefits increases the financial safety net for the surviving spouse. If Harry claims benefits at 62 and passes away, Lisa would receive only $975. If he waits until 70, she could receive up to $1,716 monthly.

Why Viewing Social Security as a Safety Net Matters

Social Security was never intended to be a complete retirement plan. It was designed as a safeguard to protect individuals from poverty, especially after losing a spouse. By delaying benefits, couples can ensure that the surviving spouse receives the highest possible monthly income, reducing financial vulnerability in later years.

Final Considerations

- Plan for the Surviving Spouse: If you or your spouse relies on Social Security for a significant portion of retirement income, consider delaying benefits to maximize survivor benefits.

- Understand the Impact of Early Claims: Claiming benefits early can permanently reduce the amount available to your surviving spouse.

- Use Other Retirement Resources: Treat Social Security as a backup rather than the main source of income.

Making informed Social Security claiming decisions can provide long-term financial security for your spouse. You can optimize your retirement strategy and protect your loved ones by viewing benefits as a safety net rather than a guaranteed income stream.

Disclaimer: This information is for educational purposes only and should not be considered legal or tax advice. Finivi Inc. makes no representations regarding the accuracy or completeness of linked third-party content and assumes no responsibility for any outcomes resulting from its use. External links do not imply endorsement.

Please consult a professional before making financial decisions. Social Security benefit amounts and regulations are subject to change. For personalized guidance, consult the Social Security Administration at www.ssa.gov.

You must be logged in to post a comment.